CDFA Exam Study Materials Q&A Latest Update 2025

Course:

CDFA

Institution:

CDFA

CDFA Exam Study Materials Q&A Latest Update 2025

After purchase, you get:

✅ Instant PDF Download

✅ Verified answer explanations

✅ Refund if not Satisfied

✅ Prepared for 2025/2026 test cycle

Document Information

| Uploaded on: | May 2, 2025 |

| Last updated: | May 12, 2025 |

| Number of pages: | 39 |

| Written in: | 2025/2026 |

| Type: | Exam (elaborations) |

| Contains: | Questions & Answers |

| Tags: | CDFA Exam Study Materials Q&A Latest Update 2025 |

Seller Information

AdelineJean

User Reviews (0)

Exam (Elaborations)

$10.00

Bundle Deal! Get all 9 docs for just $21.00

Add to Cart

100% satisfaction guarantee

Refund Upon dissatisfaction

Immediately available after purchase

Available in Both online and PDF

$10.00

| 0 sold

Discover More resources

Available in a Bundle

Content Preview

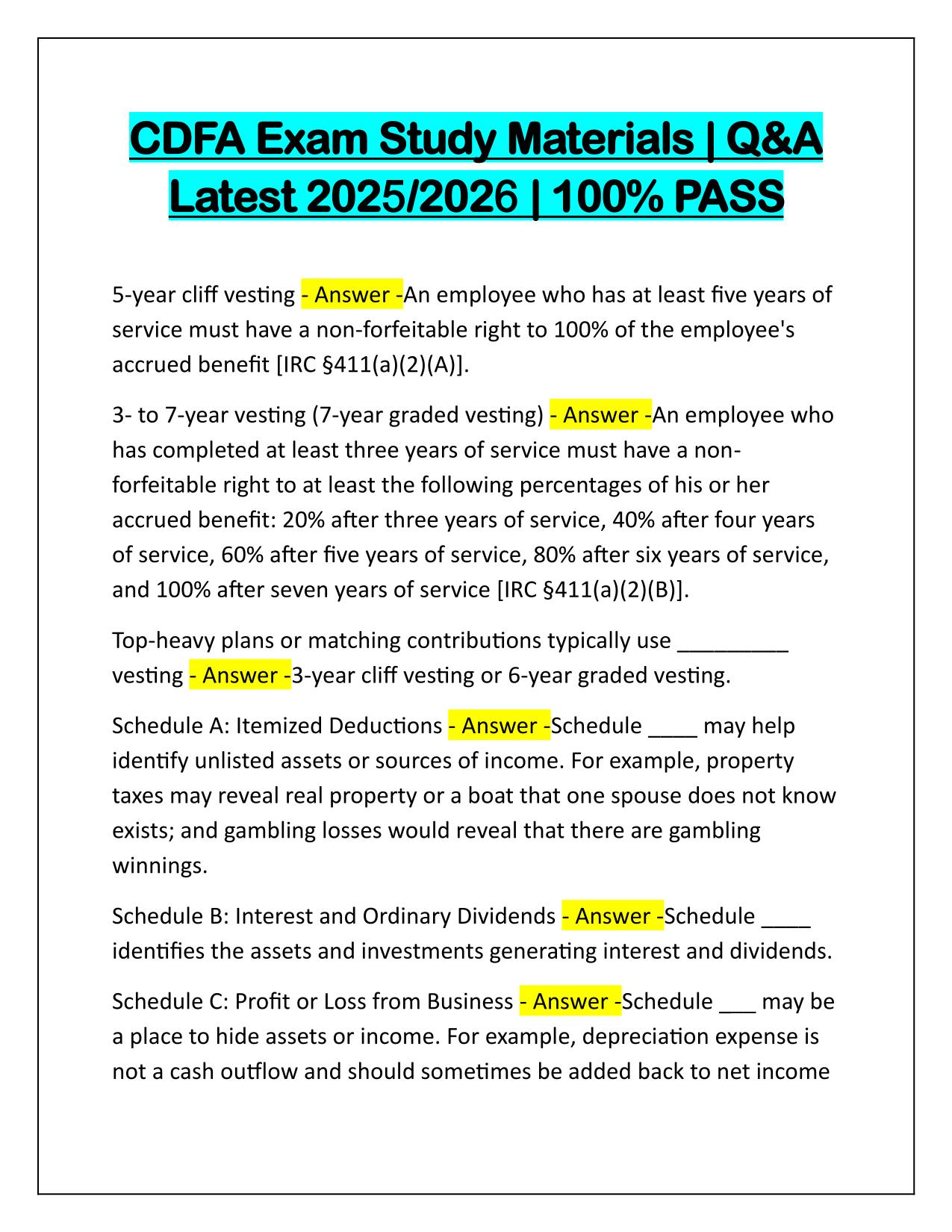

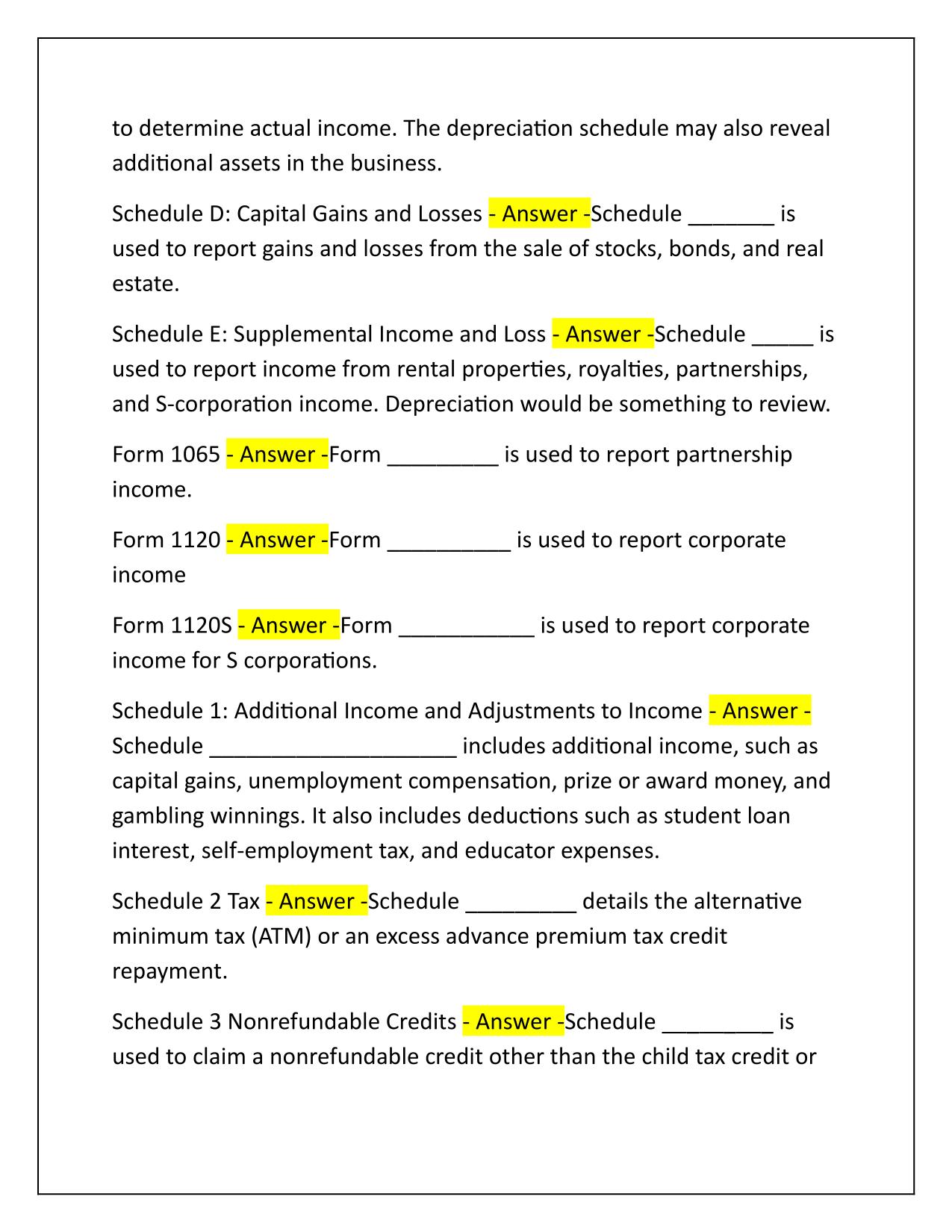

CDFA Exam Study Materials | Q&A Latest 2025/2026 | 100% PASS 5-year cliff vesting - Answer -An employee who has at least five years of service must have a non-forfeitable right to 100% of the employee's accrued benefit [IRC §411(a)(2)(A)]. 3- to 7-year vesting (7-year graded vesting) - Answer -An employee who has completed at least three years of service must have a nonforfeitable right to at least the following percentages of his or her accrued benefit: 20% after three years of service, 40% after four years of service, 60% after five years of service, 80% after six years of service, and 100% after seven years of service [IRC §411(a)(2)(B)]. Top-heavy plans or matching contributions typically use _________ vesting - Answer -3-year cliff vesting or 6-year graded vesting. Schedule A: Itemized Deductions - Answer -Schedule ____ may help identify unlisted assets or sources of income. For example, property taxes may reveal real property or a boat that one spouse does not know exists; and gambling losses would reveal that there are gambling winnings. Schedule B: Interest and Ordinary Dividends - Answer -Schedule ____ identifies the assets and investments generating interest and dividends. Schedule C: Profit or Loss from Business - Answer -Schedule ___ may be a place to hide assets or income. For example, depreciation expense is not a cash outflow and should sometimes be added back to net income

Gradesity

We are here to help

Questions? Leave a message!

Newsletter

Get notified upon new uploads. Subscribe to our Newsletter.